Is Risk Profiling Just Another

Questionnaire?

April 11, 2019

For too long, investing has lost its way. With so many financial products and hard selling, we risk paying too much for something unsuitable. It is an uneven playing field. Yet, we are to blame. Whenever people talk “investing”, almost all attention is on returns. Worse, many will get excited and join the conversation when they hear about high returns. But high returns require taking high risks, which mean high losses too! Yet, people only talk about the upside. Why? Humans are intrinsically programmed in the survival gene to be “greedy” and to fear “losing out”.

Fundamentals of Investing

Investing should be about targeting the risks first before chasing returns. I propose three fundamentals to consider.

First, returns come from taking risk - “no pain, no gain”. If two persons achieved the same return, and one took more risk than the other, who is the smarter one? Surely, it must be the one who took less risk! So risk-adjusted returns should be our focus, not returns for returns sake.

Second, decide much risk to take. But this is near impossible for humans. Emotions cloud our ability to manage risk consistently. We talk about our “wins” and remain silent about our “losses”. As primal humans programmed by greed and fear, we alternate between (i) taking more risk than we should; and (ii) taking less risk than we should. No surprises that we tend to buy high and sell low. We do not know the risks until something bad happens.

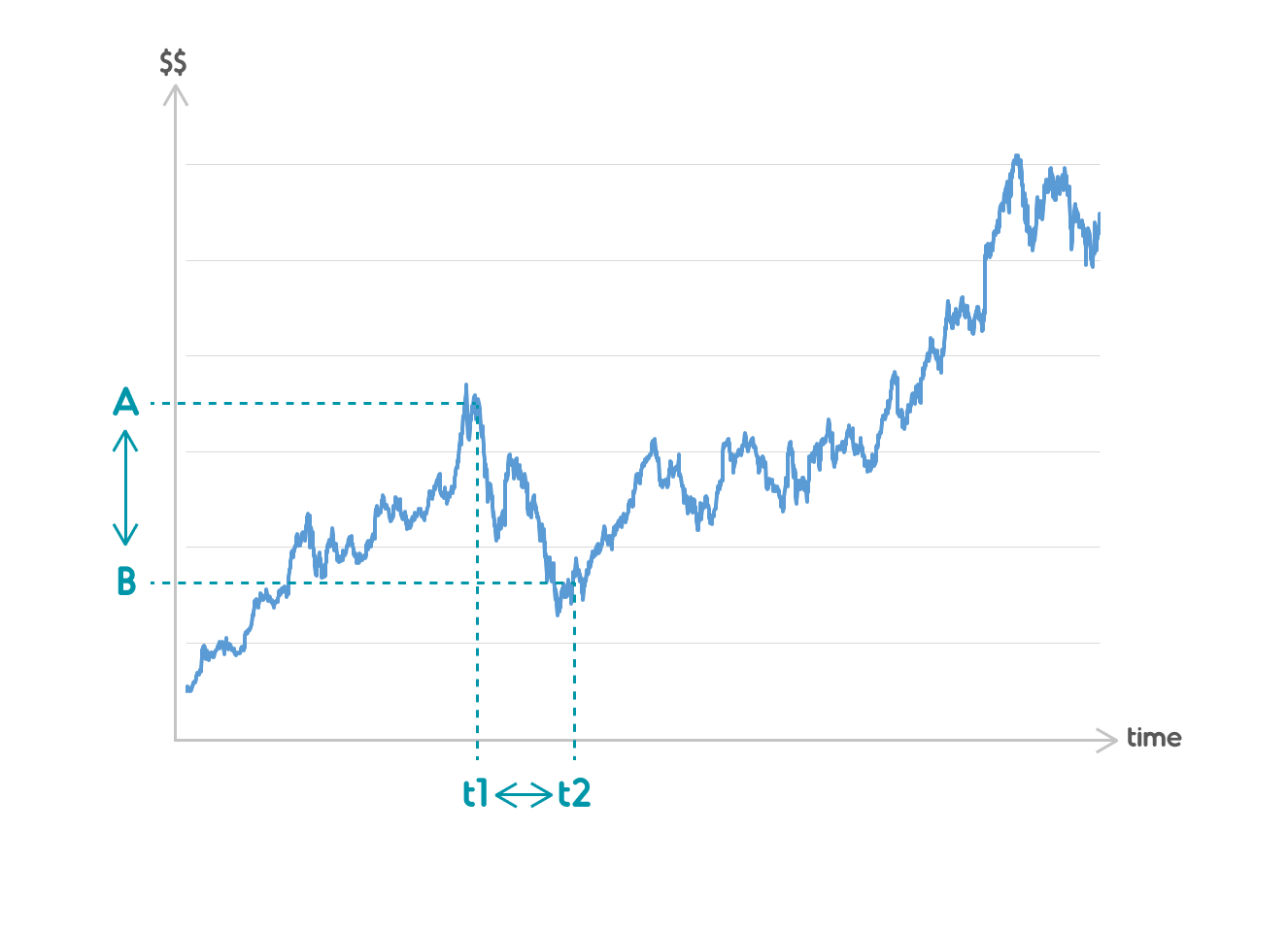

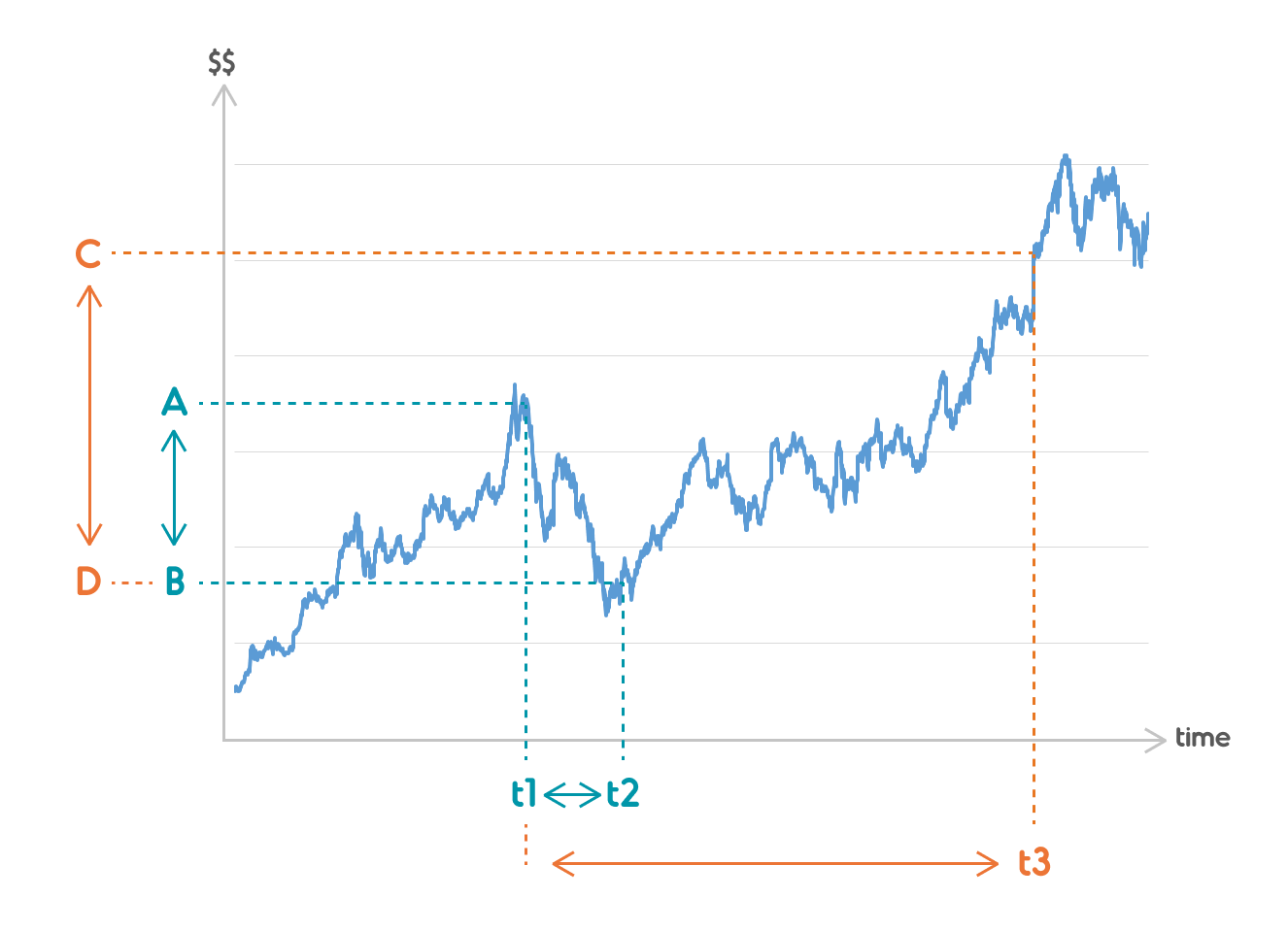

Third, time evens out risks. “Volatility” – investment risk by another name – will smooth out over a longer time. With a short-term view, there is high likelihood we will buy high and sell low (see Figure 1A).

Over a longer time, the likelihood of riding out volatility and generating a positive return is higher (see Figure 1B). Past market crashes show recovery typically within 3 years. Time smooths volatility.

Figure 1A

Figure 1B

Risk Profiling

Knowing how much risk to take varies from person to person, and from time to time. We have different personalities, different circumstances and therefore, different needs. To protect consumers, regulators require risk profiling to ensure that financial products sold are “suitable” for the consumer’s needs and risk tolerance.

In practice, risk profiling methods are typically questionnaires mechanically done as part of the intended process to sell a specific product [1]. Research shows that risk profiling questionnaires influenced less than 15% of the final choice made by investors [2]. With questionnaires subservient to the intent of selling a product, there is no consensus or validation of what an adequate risk profile is. Therefore, it is an open question if investment products sold are suitable [3].

The influence of the human salesperson is significant. A study found that questions covering time horizon, financial knowledge, income, net worth, age, gender and occupation explained only 13% of why investor portfolios were deemed suitable. However, this rose to 32% when the salesperson was included [4]. So, the salesperson influences the investor’s decisions more than the investor’s own objective considerations! This can’t be good for the consumer.

How can we improve the odds in favour of the end-consumer?

We can improve today’s human-biased practices by returning to the fundamentals of risk profiling. Risk tolerance comprises (i) Risk Capacity; and (ii) Risk Aversion.

“Risk Capacity” is the ability to take on risk and depends on the investor’s investment horizon, liquidity needs, income and wealth, among other factors.

“Risk Aversion” depends on subjective psychological traits and emotions which drives willingness to take on risk of financial loss. Such emotions are difficult to test in passive questionnaires.

“Gamification” in Risk Profiling

A better way to identify objective traits and subjective biases in each person is to assess risk-reward trade-off behaviour. The risk-reward assessment may not relate directly to real investing but can capture the inherent “irrational” personal risk-reward bias.

Risk-reward trade-offs are well studied in Game Theory. Hence, I believe there is scope to improve traditional risk profiling with gamification techniques and machine learning.

At SqSave, we apply Serious Gaming to enhance our Risk Profiling analytics. “Serious Gaming” is the discipline of game design for a primary purpose other than pure entertainment. Series Gaming is increasingly applied in education, science or health. We believe it has great potential in finance, starting with risk profiling at SqSave. Read our white paper on the SqSave Risk Profiler™ here.

SqSave Risk Profiler™ poses risk-reward dilemmas in a sequence of random outcomes based on relative potential gains and losses. By using behavioural analytics and gamification, we assess an individual’s risk profile based on actual personal choices made in every risk-reward trade-off. We see potential in applying machine learning AI techniques to our Serious Gaming approach to identify an investor’s risk profile as we accumulate more data with time.

With more data gathered through wider demographic use of our SqSave Risk Profiler™, I hope to index and track periods of heightened or dampened risk perceptions, across different objective and time-based frames. I will continue to develop new ways to capture one’s innate behaviour through applied Serious Gaming techniques not just in investing, but also in risk protection (e.g. insurance), health, lending and rewards.

Conclusion

Risk profiling is the cornerstone upon which financial advice and investment recommendations are built. Yet, the prevalent questionnaire-based risk profiling has seen little innovation to account for inadequacies found by financial behaviour research. Such questionnaires are not empirically validated nor have scientific significance to serve investor interests first. SqSave Risk Profiler™ is our innovative contribution to improve the investor odds. By overcoming the need for literacy, we will be able to serve the un(der)served with our gamified risk profiling approach. Considering the vast number of unbanked who have mobile phones and play games, SqSave Risk Profiler™ paves the way for global investing and financial inclusion.

[1] Davies, G.B., and P. Brooks. 2014. “Risk Tolerance: Essential, Behavioural and Misunderstood.” Journal of Risk Management in Financial Institutions, vol. 2: 110–113.

[2] Foerster, S., J.T. Linnainmaa, B.T. Melzer, and A. Previtero. 2014. “Retail Financial Advice: Does One Size Fit All?” NBER Working Paper No. 20712.

[3] Rice, D.F. 2005. “Variance in Risk Tolerance Measurement—Toward a Uniform Solution.” PhD Thesis, Golden Gate University.

[4] Foerster, S., J.T. Linnainmaa, B.T. Melzer, and A. Previtero. 2014. “Retail Financial Advice: Does One Size Fit All?” NBER Working Paper No. 20712.

More Articles more

What You Should Know About Unit Trusts

April 18, 2019 | Victor Lye, CFA CFP®

Not everyone has the same gung-ho risk attitude. Yet there is a fear of losing out when you hear boasts from people who say how much money they made from investing. Read more

The Good Old Days, and The Fantastic Days Ahead...

May 7, 2019 | Victor Lye, CFA CFP®

Many years ago, when I was a

stockbroker, I researched companies

listed on various stock exchanges.

Based on my research, ...

Read more

Why Replace The Human Investment Manager?

May 21, 2019 | Victor Lye, CFA CFP®

When investors ask me what I do, I cheekily tell them that I intend to replace their human investment manager. Read more